Why Singapore has no policy rate, the yen collapsed, and Brazil paid you 14% to hold a rising currency?

How Every Country Actually Runs Its Money

Exchange rates and interest rates shape our everyday lives. The exchange rate affects our purchasing power; the interest rate affects borrowing costs and asset prices. If you earn Singapore dollars, a trip to Japan looks attractive. If you buy a house in Singapore, you’ll notice the mortgage rate moves in line with rates in the United States. Yet most of us don’t know the mechanism underneath — how these variables move and interact.

The Impossible Trilemma

The impossible trilemma states that a country can have only two of three things: control of its interest rate, control of its exchange rate, and free movement of capital.

When capital flows freely, the no-arbitrage relationship between interest rates and the exchange rate is:

where S is the spot rate (domestic currency per unit of foreign), F the forward rate, i_d the domestic interest rate, and i_f the foreign rate.

The formula says: holding one unit of domestic currency (which grows to 1+i_d) must equal converting it to foreign currency at the spot (1/S), earning the foreign rate (1+i_f), and converting it back through a forward contract (F).

The equation is just a constraint — it doesn't say which variable drives the others. That's a choice. A country pins one lever, and the formula then determines the rest.

Take Singapore. The MAS uses the exchange rate, not the interest rate, as its main policy tool — managing the Singapore dollar against a trade-weighted basket (the S$NEER) within a band, usually on a gently appreciating path. When the market expects the Singapore dollar to strengthen, the formula does the rest: F < S , so F/S<1, which pushes SGD interest rates below foreign rates. The MAS never sets the domestic rate directly — it falls out of the currency policy.

But here’s the crucial limit: this formula pins down the forward rate, not the future spot rate. The forward is locked in by covered arbitrage; where the spot actually goes depends on expectations, risk premia, capital flows, and policy credibility.

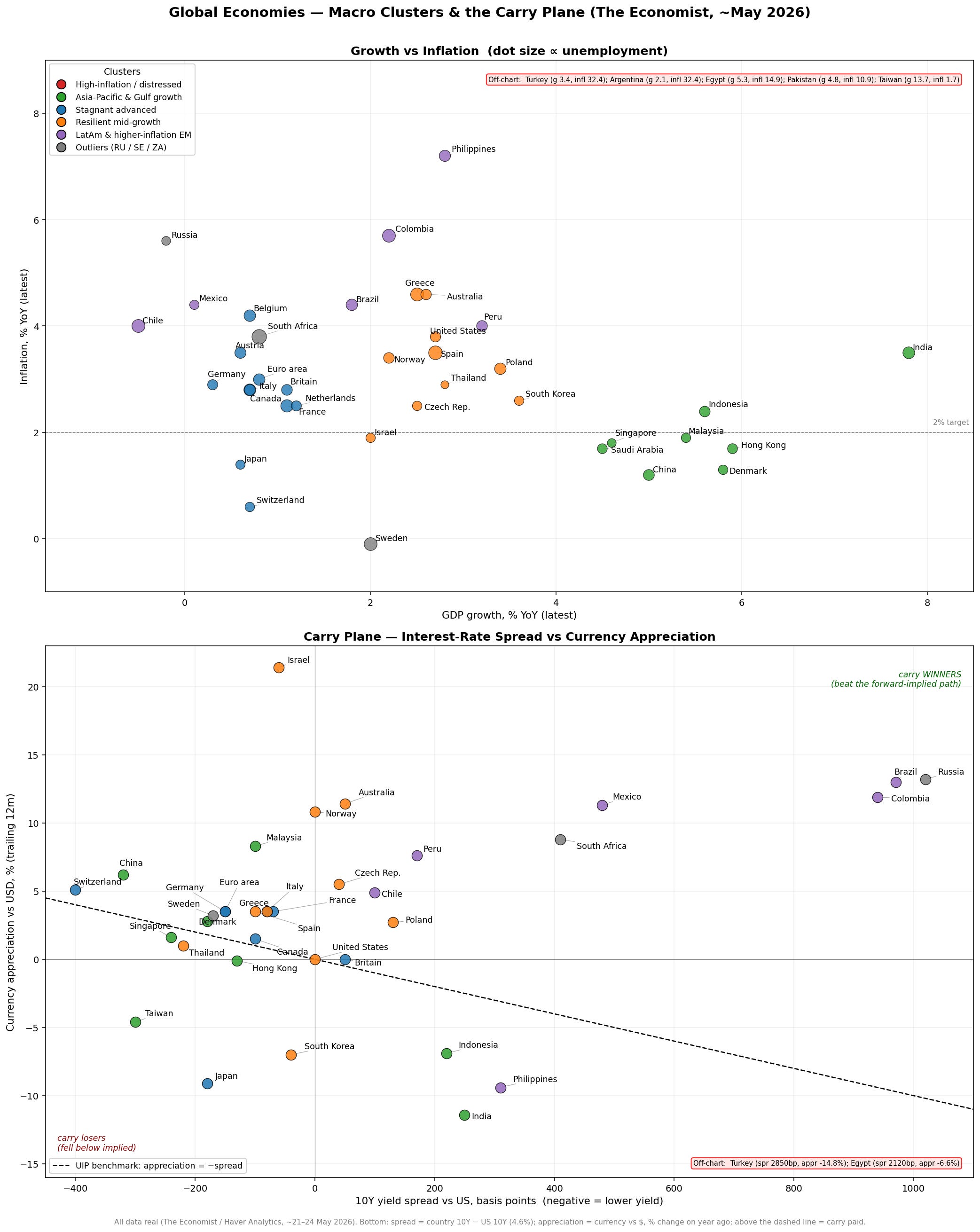

Japan makes the point. Its interest rate is far below the United States’. The formula puts the yen at a forward premium — so you might expect it to strengthen. In reality, the yen depreciates.

Covered and Uncovered Interest Parity

The formula above is covered interest parity — “covered” because you hedge the currency risk with a forward. It’s a no-arbitrage benchmark, and in deep, liquid markets it holds very closely. (It can drift only when funding stress or balance-sheet constraints open a “cross-currency basis,” as they have at times since 2008.) But notice what it does and doesn’t say: it pins the forward price to the interest-rate gap. It says nothing about where the spot rate will actually go.

That second question belongs to uncovered interest parity — the unhedged version. In theory, a low-yielding currency should appreciate just enough to offset its lower interest rate. In practice this often fails, because investors demand risk premia, chase carry, or react to safe-haven and policy shifts.

Japan is the clearest case. Its low rate puts the yen at a forward premium, but in the spot market traders borrow cheap yen to buy higher-yielding foreign assets, creating selling pressure that pushes the yen down. Switzerland shows the other side: despite equally low rates, the franc tends to appreciate, because it enjoys safe-haven demand.

Notice the pattern: the same low interest rate sends the yen down and the franc up. The interest rate alone never tells you which way a currency moves — what matters is which lever the country chose to control, and what it leaves to the market.

Around the World

China has restricted the free flow of capital, which lets it steer both the interest rate and the exchange rate more independently — because the arbitrage channel that would otherwise link them is constrained. The link isn’t fully severed (trade flows, approved investment channels, and the offshore CNH market still matter), but it’s loose enough that domestic rates and the yuan can diverge from what open-market arbitrage would dictate.

Taiwan faces recurring appreciation pressure from its strong external position and capital inflows. To lean against excessive TWD appreciation and protect export competitiveness, its central bank buys foreign currency and accumulates reserves (now over US$600 billion), while using monetary and prudential tools to manage domestic liquidity.

Brazil, as of 2026, shows the opposite of Japan. With a high policy rate, the real’s forwards imply depreciation under interest parity — yet the spot real has appreciated, because high carry, improved sentiment, and capital inflows more than offset the forward-implied decline.

Closing

Three levers — interest rate, exchange rate, free capital — and you can pin only two. The third is whatever the market makes of it. So the next time your Singapore mortgage tracks the Fed, or your yen holiday gets cheaper, you’re watching the same equation at work — quietly linking interest rates, exchange rates, and the flow of capital across the world.